The Economy Right Now

End of Q3 update on jobs, prices, and markets

Business Cycle Position Today

The economy is still growing, but slower. Services are steady. Factories are soft. Hiring has cooled. Inflation is moderate. The Fed has started cutting to keep growth from slipping.

Jobs and wages: Hiring is positive but smaller than earlier in the year. Unemployment has nudged higher. That means the labor market is loosening, not collapsing. Average hours worked are basically flat, which fits the same story.

Spending: Consumers are still spending. Recent monthly growth in personal consumption was solid. That can continue for a while, but it is not a forever pace.

Factories and services: Manufacturing sits in mild contraction. Services, which are the larger share of the economy, are still expanding. Inside services, new orders look fine while hiring has cooled. In plain English, people and companies are still buying, but managers are slower to add staff.

Policy shift: The Fed cut rates in September. The interest on reserve balances is lower now. That is a move from tight toward easier policy. This is common late in an expansion when growth is slowing.

· Phase signals right now.

o Expansion traits are still present in services and consumer spending.

o Peak traits are visible because unemployment is no longer falling and the Fed has pivoted to easing.

o Contraction traits are partial. Manufacturing is below 50 and service sector hiring has cooled.

o Trough traits are not present. Credit spreads are not blowing out and markets are not in panic.

o Net result: late-cycle expansion with a soft-landing attempt. Growth is slower but positive, and policy is leaning supportive instead of restrictive.

The Economic Machine

The United States is in a late-cycle expansion with three big gears moving at once. Productivity looks better than last year. Credit is available but not loose. Confidence has slipped.

Productivity:

Output per worker jumped in the spring. Nonfarm business productivity rose at a 3.3 percent annual rate in Q2 2025, while unit labor costs rose only 1.0 percent. That combo says firms are squeezing more output from each hour worked, which helps profits and keeps price pressure contained.

Credit:

Banks are still careful. The Fed’s July lending survey says standards stayed on the tight side and demand for business loans was weaker, especially for commercial and industrial loans. For households, mortgage standards were basically unchanged, credit card standards tightened a bit, and demand for most consumer loans cooled. Banks also said today’s standards sit toward the tight end of their own long-run ranges.

Consumers are still borrowing, just not at a breakneck pace. In July, total consumer credit rose at a 3.8 percent annual rate. Revolving balances like credit cards rose at a 9.7 percent annual rate. Nonrevolving credit rose 1.8 percent.

Psychology:

Mood got shakier in September. The University of Michigan sentiment index fell to 55.1 from 58.2 in August. People cited price fatigue and a cooler job market. The Conference Board said August confidence was little changed, which fits the picture of an economy that feels slower but not broken. Retail investor mood is near neutral. AAII’s latest read shows a small bull minus bear spread of about 2.5 percent.

Summary:

Productivity is a bright spot. Credit is cautious but functioning. Psychology is fragile. Put together, that is consistent with a late-cycle expansion that can keep going if jobs and credit remain orderly.

Credit & Liquidity Pulse

Credit markets look calm. Liquidity is tighter than 2023 but still working. The dollar firmed into quarter end.

Spreads:

Risk pricing is not flashing trouble. U.S. high-yield spreads sit around 2.8 percentage points over Treasuries, which is tight by historical standards. Investment-grade spreads are near three quarters of a point. That is consistent with “orderly” rather than “stress.”

Issuance and demand:

Companies have been able to sell a lot of bonds into this strength. September investment-grade supply was on track to set a monthly record, with a single-day jumbo deal from Oracle a good example. Bond ETF inflows picked up alongside tighter spreads.

Fed balance sheet and money plumbing:

The Fed’s total assets were about 6.61 trillion dollars on September 24. That confirms quantitative tightening is still in place, only slowly shrinking reserves. Use of the Fed’s overnight reverse-repo facility fell to the lowest level since 2021 earlier this month, which tells you excess cash parked at the Fed has drained back into bills and markets.

Money supply:

M2 ticked higher through the summer. The August reading was 22.20 trillion dollars. After the big decline in 2022 and 2023, 2025 has looked more stable to slightly higher.

Dollar:

The dollar index hovered in the high 97s to low 98s late this week and was set for a second weekly gain. A firmer dollar usually tightens global financial conditions a little at the margin.

Summary:

Credit is open and priced for a soft landing, not a shock. Liquidity is tighter than during the peak stimulus years but is functioning. If spreads were to jump and reverse-repo usage were to rise sharply, that would change the story. For now the backdrop supports a late-cycle expansion rather than a credit crunch.

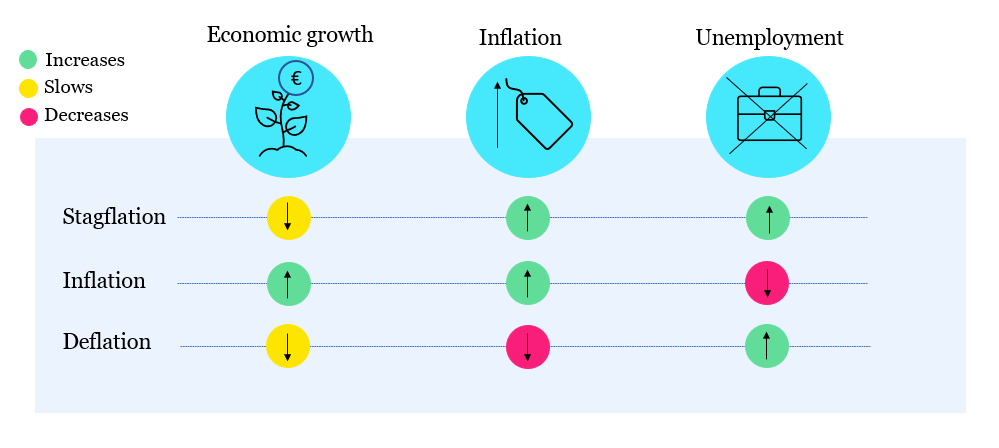

Inflation, Deflation, Stagflation

Where prices stand now:

Inflation is moderate. The CPI report for August showed 2.9 percent year over year, with core CPI at 3.1 percent. The Fed’s preferred gauge, PCE, was 2.7 percent year over year in August. Core PCE was 2.9 percent. Monthly moves were small and lined up with expectations. This says prices are not falling, but they are not racing higher either.

Read on risk mix:

Deflation is not present because prices are rising and credit markets are calm. Stagflation is not the base case because growth is still positive and services are expanding. If the labor market softened quickly and inflation stayed sticky, that would push the risk toward stagflation. For now the data point to late cycle expansion with moderate inflation.

Simple tilt rules, not advice:

Inflation tilt favors energy, commodities, real assets, and gold.

Deflation tilt favors cash and high quality bonds.

Stagflation tilt favors hard assets, some real estate, and selective crypto.

Markets Lead the Economy

How the tape is acting:

The yield curve has moved back above zero this month on the 10 year minus 2 year spread. That usually happens when the Fed shifts toward easier policy and the market starts to price a reset in growth. Stocks pulled back in September but credit stayed calm. Volatility has bounced around data days, but there are no crisis signs in the standard stress gauges.

Why this matters:

Markets move first. Headlines catch up later. When you finally see big confirmation headlines, a large part of the move is usually already done.

Sector Rotation Now

Old playbook, new twist:

The classic flow is cyclicals to industrials and materials to commodities and energy to defensives, then back to cyclicals. Today there is a clear split inside technology. Must have spend in AI chips, cloud infrastructure, and core e-commerce tooling has held up better than nice to have software. That shows up in company commentary and in stronger services activity. The August ISM Services report showed business activity at 55 and new orders at 56, while hiring inside services was softer at 46.5. That mix fits a late cycle expansion where buyers stay active and managers pace hiring.

Lets Put It All Together

How the main signals line up right now.

Yield curve. Slightly positive on the 10 year minus 2 year spread after a long inversion. That is consistent with a policy turn and a reset phase.

PMIs. Manufacturing is in mild contraction at 48.7. Services is expanding at 52 with firm new orders and softer hiring. That is a mixed but workable setup.

Credit spreads. High yield and investment grade option adjusted spreads are still tight. That says stress is low.

Labor pulse. The unemployment rate is 4.3 percent and August payrolls rose by about 22,000. Cooling, not breaking.

Net read.

These pieces together say late cycle expansion with a soft landing attempt, not a hard landing. The overlapping signals are more important than any single print.

Sentiment & Headlines

Where mood sits.

Consumer sentiment fell in September. The University of Michigan headline index dropped to 55.1 as people cited price fatigue and a cooler job market. Retail investor mood is near neutral. AAII showed about 41.7 percent bullish and 39.2 percent bearish in the latest read. Mood is not euphoric and not in panic either.

How to use it.

When headlines feel euphoric, risk should usually be trimmed. When headlines feel catastrophic, risk can usually be added carefully. The crowd tends to react late.

Crypto Cycle

State of play:

$BTC is trading near $109,000. $ETH is near $4,000. Both pulled back from recent highs but remain in uptrends on a multi quarter view.

Cycle lens:

We are in the post halving phase for Bitcoin. In past cycles the market has still had sharp shakeouts inside the larger advance. On chain and derivatives gauges help time risk, but the big picture is simple. Supply growth is slower than before, demand is cyclical, and price action is noisy.

What matters most for the next leg:

If risk appetite in equities stays healthy and credit remains calm, crypto tends to do better. If funding markets or credit spreads flash stress, crypto usually takes the hit first.

Summary

Across these sections the story is consistent. The United States is in a late cycle expansion. Growth is slower, policy is easing, credit is orderly, and mood is cautious. That mix supports a soft landing path with choppy markets rather than a hard break.