Weekly Macroview and Game Plan

Sep 8, 2025

How last week’s Macro View played out

Before we get into this weeks macro view, let’s see how last weeks macro view aged.

Last week’s macro view called for new S&P all-time highs ahead of FOMC and they arrived. Calls had edge while ~6,500 held ($ES), and that buy-the-dip framework worked as small-caps took the baton into Friday. Tech didn’t clear the 580–583 gate on $QQQ, so that remains the momentum tell. With the Fed in blackout and CPI up next, the next leg is data-led. These plans are delivered each weekend.

Lets get into this week’s Macroview

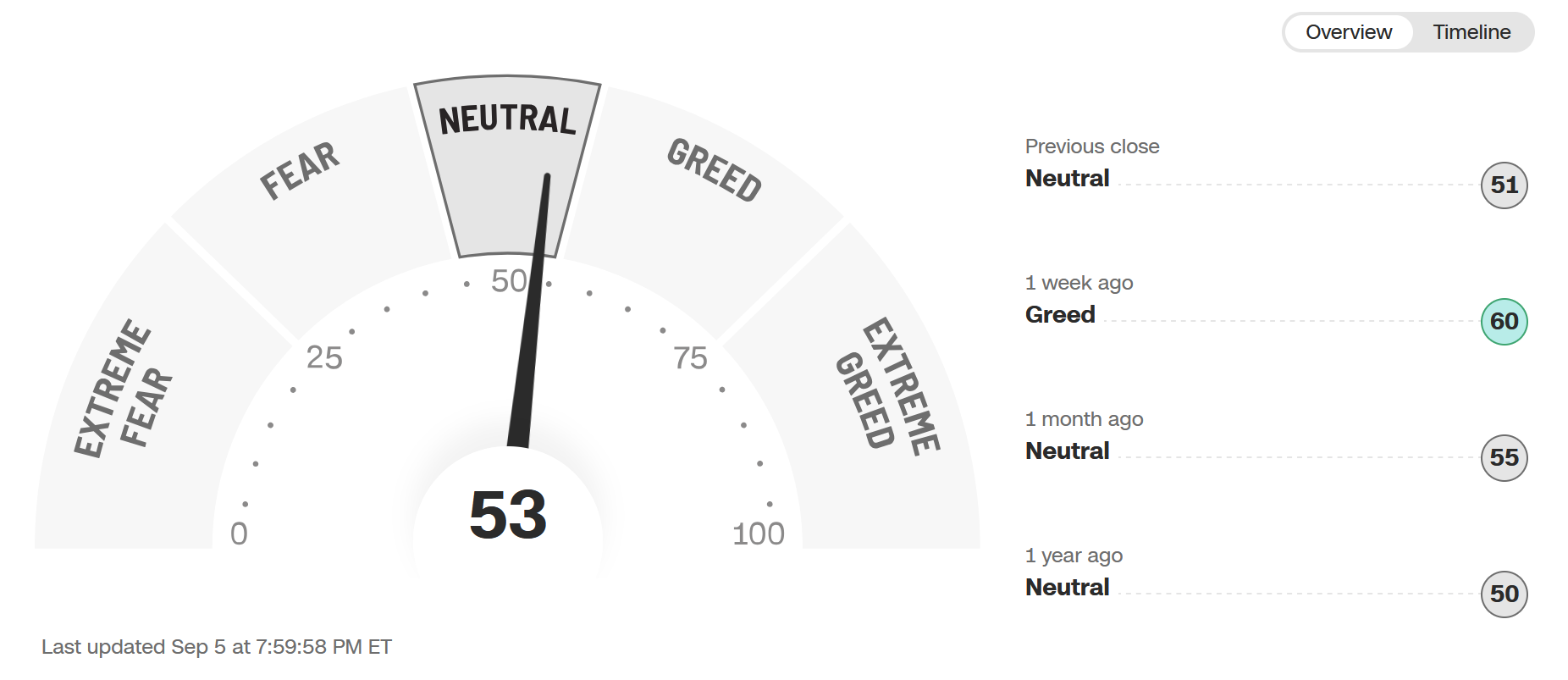

Sentiment first: Fear & Greed

The tape isn’t stretched. Fear & Greed sits around 53 (Neutral) a come-down from last week’s “Greed,” and right in the zone where data can push the market either direction. That’s constructive into a catalyst-heavy week because it lowers the odds of an abrupt mean-reversion on sentiment alone.

Trend check: where the charts stand

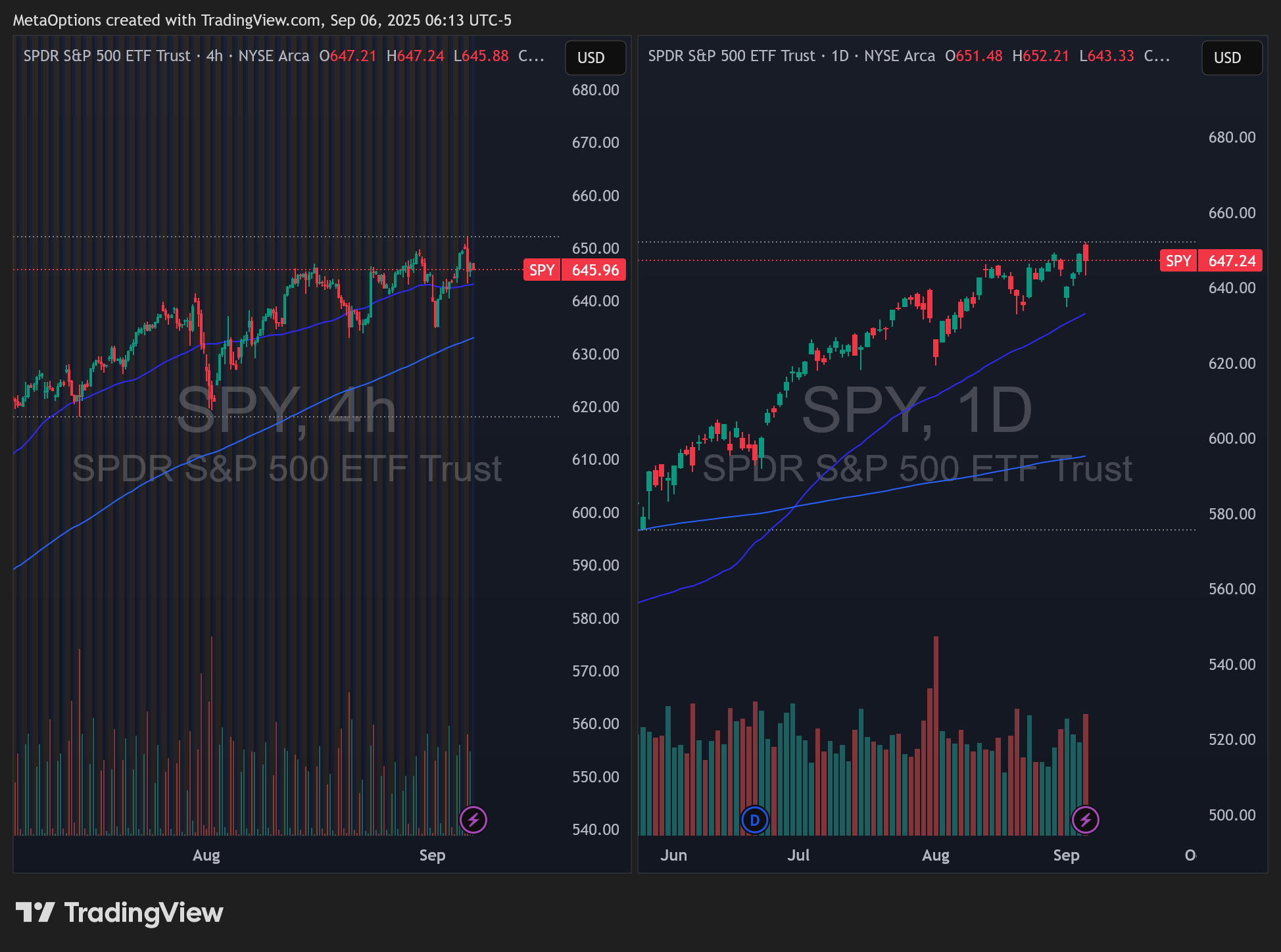

$SPY pulled back from fresh highs but still rides above rising 50-day/4-hour averages;

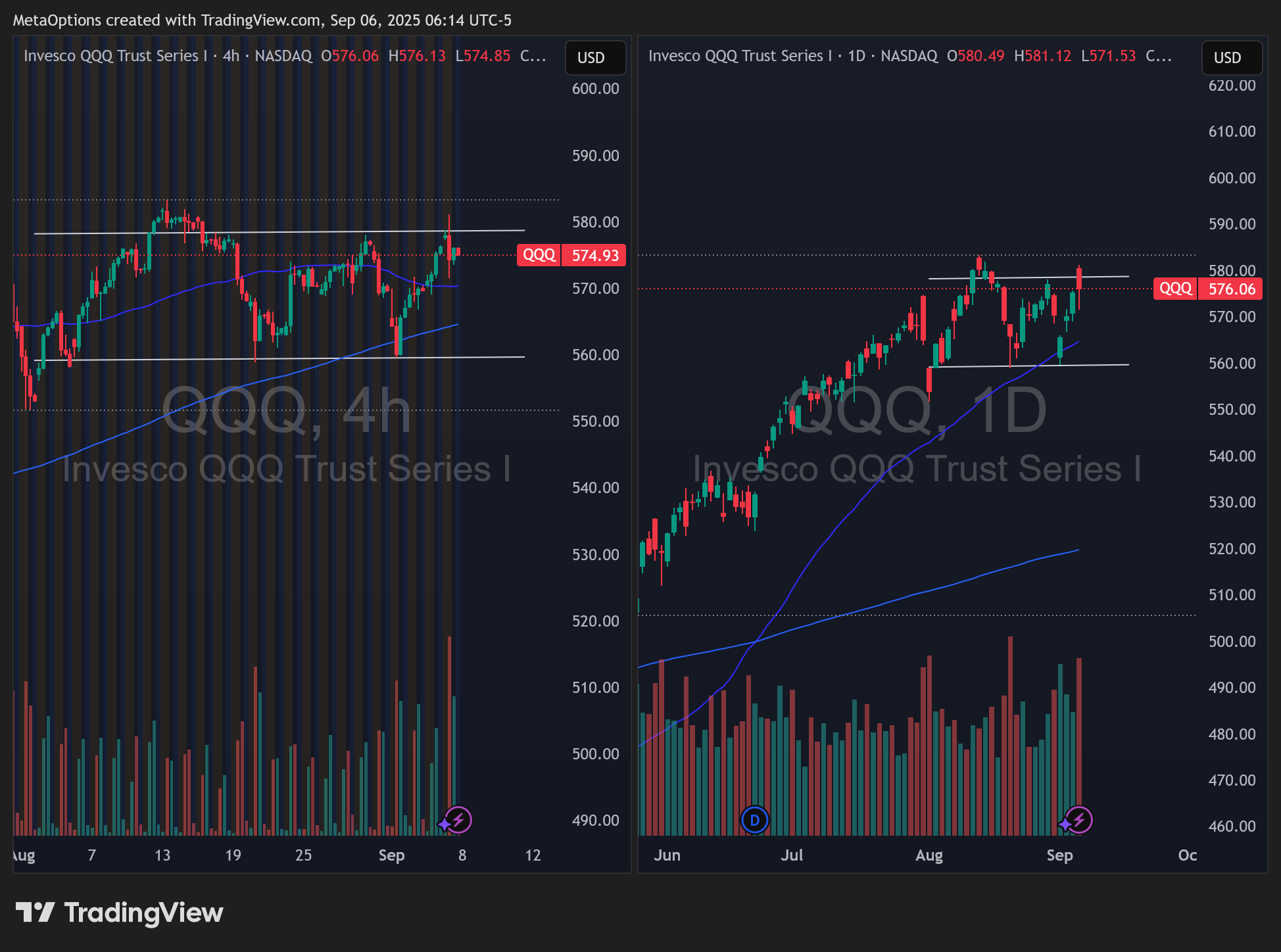

$QQQ has reclaimed its 50-day with 572–575 as the nearby battleground and 580 as the momentum trigger;

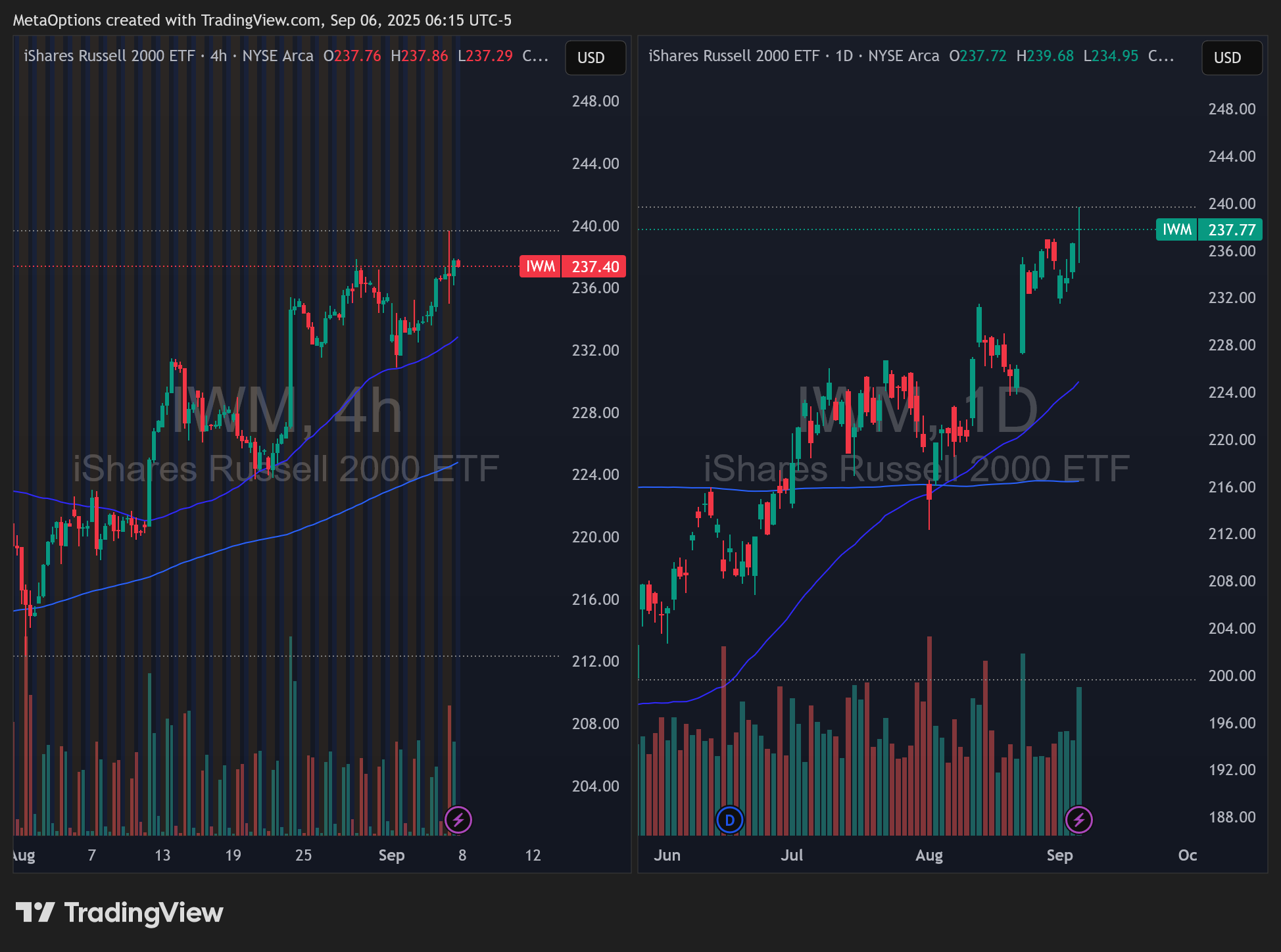

$IWM is pressing prior highs and leading on both daily and 4-hour time-frames. If small-caps keep leading, breadth remains a tailwind.

The week ahead: the catalysts that matter

Two clusters drive the narrative: inflation prints and the Fed.

Inflation

• PPI (Aug) — Wed, Sep 10, 8:30a ET.

• CPI (Aug) — Thu, Sep 11, 8:30a ET.

Markets will key on core goods vs. shelter and any energy impulse.Growth & sentiment

• Univ. of Michigan Consumer Sentiment (Sep prelim) — Fri, Sep 12, 10:00a ET. Watch inflation expectations components.Spending

• Retail Sales (Aug) — Tue, Sep 16, 8:30a ET. A hot control-group print would complicate a dovish Fed pivot.Policy

• FOMC (Sep 16–17) with a new SEP and press conference on the 17th. We’re already in the Fed blackout window (started Sat, Sep 6), so no official jawboning into the meeting.Flows

• Quarterly options expiration (“triple/quad witching”) — Fri, Sep 19. Expect heavier volume, potential pinning, and dealer-flow cross-currents.Index mechanics

• S&P 500 adds: Robinhood ($HOOD), AppLovin ($APP), Emcor ($EME) effective Mon, Sep 22 pre-open. Passive flows and hedging around these changes can create idiosyncratic volatility.

Miscellaneous

Cuts are coming but size is now in play. After the weak August jobs report (22k payrolls, unemployment up to 4.3%), desks now expect the Fed to begin an easing cycle in September; the debate is 25bp vs. 50bp. Markets lean 25bp but allow a tail for 50bp if inflation cools further or growth cracks.

Morgan Stanley (Mike Wilson): buy dips into cuts. Wilson argues equities typically perform well during cutting cycles, sees room for small-caps if the Fed gets ahead of the slowdown, and recommends leaning into September weakness rather than fading it. The thing he leaves out is the magnitude of cuts and why they are being made. If FED starts cutting heavy and fast, then I would be apprehensive to buy the dips vs. easing into cuts like planned.

Goldman Sachs (Paolo Schiavone): “buy the September dip.” House view looks for the S&P 500 to 6,700–6,900 as rate cuts support multiples and growth re-accelerates—tactically constructive unless CPI surprises hot.

Exogenous risks to keep on the radar

OPEC+ supply path: Saudi Arabia is pressing to accelerate the next output increase. A faster unwind of cuts would lean on crude, help headline CPI later but near-term energy volatility can still whipsaw risk.

Seasonality & flow: September’s reputation as the weakest month is well-worn, and witching week can amplify moves. With daily options prevalent, expiries sometimes have less directional bite but intraday pinning around big strikes remains common.

How it nets out

Setup: Sentiment is neutral, breadth is improving ($IWM leadership), and the trend is intact but a CPI/PPI → FOMC gauntlet means event risk is elevated. If CPI is benign, the path of least resistance is a grind higher into/through the Fed as “cuts begin” becomes baseline. A hot CPI would revive the “50bp vs. 25bp” debate in the wrong direction for duration-sensitive tech and could trigger a shakeout into witching.

Levels from the charts (for framing, not prophecy):

SPY: 645–648 = pivot; 640/633 (50-DMA) as downside context.

QQQ: 572–575 = intraday battleground; 580+ opens momentum; 565 (50-DMA) as support.

IWM: 237–239 = resistance to watch; sustained breakout strengthens the breadth bull case.

Trading bias (CSP/short-vol lens): With F&G neutral and catalysts stacked, sizing is the risk lever. I favor selling below rising 50-day levels on names I like, but keep notional light until CPI/FOMC are behind us and be mindful of Friday-to-Friday pin risk into witching.